The Entryway: Q4 2025 Market Update & Outlook

Market Snapshot:

As we near the conclusion of 2025, we are continuing to see overall strength in asset prices as equity markets have continued their march higher after the “tariff tantrum” during April 2025 – led by large-cap technology stocks. The Bond market has continued to rally as the Federal Reserve has cut interest rates twice with likely more interest rate cuts to come, and the IPO / secondary markets have shown a notable rebound in 2025.

While asset prices are continuing to climb, there continues to be conversation over the concentration within the equity markets. For instance, the S&P 500 is a diverse index representing the 500 largest publicly traded companies in the United States. These 500 companies represent all sectors of our economy, but if you look at the overall performance of the individual companies within this index you find that this “diverse basket” is really being driven by only 7 companies, aka “The Magnificent 7” (Apple, Microsoft, Alphabet, Amazon, Meta, Nvidia, and Tesla).

On the one hand, this is concerning as the Magnificent 7 represent ~37% of the total market cap of the S&P 500 (a level not seen since the 1960s) and are heavily contributing to the indexes’ recent returns. The Mag 7 made up the following percentage of the overall returns of the S&P 500 over the last several years: 2023 = 60%; 2024 = 55%; YTD (2025) = 58%. While returns have been robust since 2023, the concentration of those returns is causing some to question the health of the overall market.

On the other hand, these are real companies with unique products and services consumers continue to value and purchase. And these companies are mostly led by generational founders or leaders that operate efficiently and turn those revenues into earnings. And at the end of the day, the stock market is driven by company earnings and their expected growth.

As of Q3 2025, the Mag 7 companies achieved 15% year-over-year earnings growth vs. 6.7% earnings growth for the other 493 companies in the S&P 500. Recently, investors have been willing to pay more for these earnings (and their growth) pushing the values of these companies higher. Today, the combined market value of these seven companies accounts for ~$22 trillion of market value. To put that in perspective, $22 trillion is more than the total annual GDP of China (2nd largest economy on Earth) and more than the annual GDP of Germany, India, Japan, UK, France, and Italy, combined.

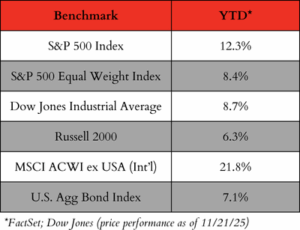

Currently, it is fair to say that as the Magnificent 7 go, the market goes. Here is where we stand as of the time of this writing:

Market Update:

While there has been some recent choppiness and selling pressure in markets, it continues to be a mostly positive year for asset prices. The real question is who owns the assets? The answer to that question generally determines your perception of the economy, your overall buying power, and your willingness to spend. Spending is important as it represents ~70% of U.S. gross domestic product (GDP) and is the largest driver within the U.S. economy.

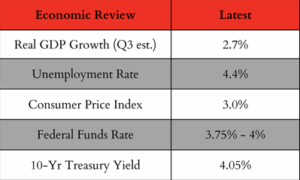

At a high level, the overall health of the US economy seems solid as we are still experiencing above average economic growth, historically low unemployment, a resilient consumer, higher asset prices, and explosive innovation in a variety of areas – lead by the development of artificial intelligence. While we believe the overall health of the US economy is relatively resilient, we do believe there is becoming a wider separation between those who own assets and those who don’t. Those that own assets have seen their balance sheets & incomes outpace inflation and in turn have a propensity to spend vs. those that don’t own assets and are financing purchases with debt. In short, the U.S. economy feels different depending on who you ask, and we are starting to see some cracks in both the labor market and with the consumer (known as the K-shaped economy).

Let’s start with the consumer. While many companies reporting Q3 2025 results saw steady demand, the general consumer continues to show a preference for value-driven segments vs. premium categories. For instance, Q3 data suggests that private label grocery sales grew 4.4% year-over-year vs. 1% growth in national brand items. In addition, private labels reached all-time highs in market share, capturing ~25% of unit sales as consumers showed a preference for value.

This “K-shaped economy” was further underscored in Q3 earnings where there was continued strength in discount retailers like: Walmart, TJ Maxx, Five Below, etc. vs. high-end luxury retailers. To us this continues to paint a picture of two different economies reflecting two different growth patterns, with affluent consumers driving robust spending on certain high-end items, while younger generations and/or those burdened with debt experience heightened financial stress. This financial stress is leading to delayed payments.

According to the Federal Reserve Bank of New York’s Household Debt and Credit Report, the national average delinquency rate on auto loans sits at 5.02% which is 40% higher than the long-term average of 3.56% and delinquency rates on credit cards for both the highest-income 10% of ZIP codes as well as delinquency rates for the lowest-income 10% of ZIP codes have increased materially since their recent lows in 2022.

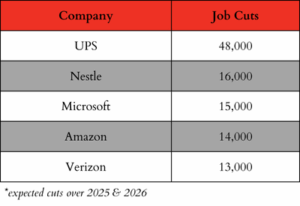

In addition to the consumer, there have been several announcements from large publicly traded companies that made recent headlines. For example, here are the intended layoffs for several large publicly traded companies over the next several years:

To be clear, these companies still collectively employ ~2.5 million people and many companies are continuing to “right-size” their employment base after over-hiring during the COVID time period, but the combination of announced layoffs and reports of hiring slowdowns within certain age cohorts is something we are watching closely.

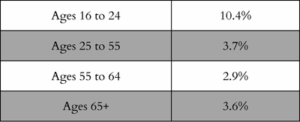

For example, while the unemployment rate is still hovering around 4.4%, and meaningfully below the 6% – 6.5% fifty-year average, there is an emerging trend of higher unemployment rates for young workers ages 16 – 24, even if college educated. Here is the current breakdown of U.S. employment by age group:

This emerging trend is producing a passionate debate as to why younger, college educated people are having trouble finding jobs. Some believe this is merely companies shedding jobs after over-hiring post- COVID and being cautious for any upcoming economic slowdown. Others believe this is a sign of companies implementing improved technology and AI systems to replace entry-level workers.

Time will tell which is more accurate, and the truth likely lies somewhere in the middle. However, it is objectively true company CEOs believe in the power of artificial intelligence, the efficiencies these systems can provide, and their potential power to unlock massive productivity gains, higher GDP growth, new products and services, drug discoveries, and an overall higher quality life.

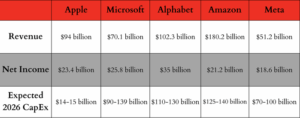

The “AI race” is best seen within these “hyperscalers” who have the existing computing infrastructure to serve millions of customers, power entire internet ecosystems, and influence the future of this technology. These companies are not only discussing how to change the world, but they are dedicating unprecedented resources (revenues / profits) to gain market dominance.

Here are the recent quarterly results for the main “hyperscalers” in the US – their revenue, profits, and expected spend over the next 12 months:

A Constant Reminder:

Markets, the economy, the newest technologies, etc. are fun to talk about and critically important for a variety of reasons. However, the dynamics of markets / the economy and the uncertainties of the day can become overwhelming if that’s where you allocate the majority of your time, energy, and efforts.

As we constantly remind our team and our clients, we must also heavily focus on what we can control as our main job is to protect our families the best we can from market volatility and emotional mistakes. To that end, we spend much of our time listening, asking thoughtful questions and building a process around those needs. These processes are the foundational elements of what we do and are what empower our clients to stay the course and consistently make logical decisions. Here are some great reminders:

First, control the controllables. This starts with having transparent and direct conversations. We must understand where you are and where you want to go and this starts with candid conversations.

Second, stay patient and stay disciplined. Money, markets, the economy, new technologies, etc. are emotional and they will constantly change. However, don’t let change or things out of your control negatively influence your peace of mind and improperly influence your decision-making. As long as we are collectively working together and having honest conversations, we can continue to develop and implement disciplined processes that will keep you and your family on track to meet your goals.

Lastly, communicate. One of the only guarantees in life is change. Change is inevitable and it can be empowering if planned appropriately. We feel confident in the people we have within our firm to deliver solutions for the families we serve but we must know what problem or goal we are working to solve.

Thank you and Welcome!

In closing, we want to thank you for your trust, and we are grateful for the opportunity to serve you and your families. We work incredibly hard to attract and retain great individuals who exhibit the entrepreneurial spirit, relentless drive, and servants heart we’re looking for within our firm. Our people and our culture are critical to our collective success and we are happy to share a few new additions to our family.