The Entryway: Q3 2025 Market Updates & Outlook

Market Snapshot:

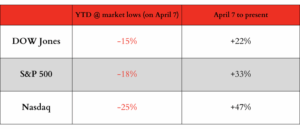

A lot has happened since our last update in early April. As a reminder, when we published our last commentary on April 7, a total of $6.6 trillion of market value had been lost by U.S. companies, the S&P 500 and Dow Jones Industrial Average ended in correction territory, and the Nasdaq composite was in a bear market. From April 7 to present, the following events unfolded: the Gaza war intensified after a ceasefire breakdown, some of the most aggressive tariffs in modern history were introduced/modified/delayed/partially implemented, and the U.S. bombed Iran’s nuclear facilities via a covert mission. Despite these added uncertainties, the S&P 500 has added about $8 trillion of market value from its April 7 market lows to present. At the time of this writing, here is where the major U.S. stock indices were vs. where they are today:

Like everyone else, we cannot predict the future. We believe this is the latest example of how not making emotional decisions and sticking to your specific plan benefits you over the long term. Our team is constantly analyzing current events, economic news/updates, specific companies and investment opportunities, overall market sentiment and more. As you or the market give us new data points, we will evolve our plan and strategies to put you in the best position for success. But we do believe it is important for everyone to recognize what they can and cannot control. The more experience we all gain, the brighter the realization is that the world and our surroundings are more complicated than they lead on. It can be overwhelming, confusing and disconcerting if you let the unknowns of tomorrow negatively influence your plan and the action items you can control. It is our job to cut through that noise and provide a consistent voice that empowers you to make good decisions.

Market Update:

As we mentioned in our prior letter, we are believers in true free trade, and we believe it is objectively true that global imbalances have built up over the last 50 years. While we all may have opinions on the execution of the administration’s tariff policies, we do believe a rebalance of trade was in order and the intent of the administration’s tariff policies is attempting to right-size some of these imbalances to more “fair trade.” Additionally, we continue to believe that if we can get to these “freer” trade policies, then the U.S. will likely come out of the other side better off. Our hope is that these negotiations continue to progress, and the administration can continue to execute trade deals to build upon the handful that have already been agreed to. While the market is currently looking through all these uncertainties, our leaders must execute in a timely manner to give business owners and consumers clarity to make informed, long-term decisions for their people, companies and communities.

Our current highest probability outcome is that we will continue to negotiate these tariffs to reasonable levels with our largest trade partners, avoid a recession and markets will continue to respond favorably – while a little choppy – along the way. The bottom line is that overall tariff rates are coming down to more reasonable levels, and the administration is allowing for numerous carve outs with various trading partners and continuing to offer incentives to invest in America while maintaining the strategic importance of mission-critical assets we must have control over (i.e., AI/chips, energy, rare earths, pharmaceuticals, etc.).

In addition, the U.S. has many favorable factors right now: historically low unemployment, a decently strong economy (and consumer) and interest rates at levels where consumers and businesses can operate efficiently but high enough where we can cut to stimulate, if needed. Lastly, the odds of Fed interest rate cuts have greatly increased recently with prediction markets assigning a ~94% probability of a 0.25% rate cut at the Fed’s September meeting. Any rate cuts would likely be positive for asset prices and may unlock pent-up demand in the housing market, which represents a large component of the United States’ GDP.

While we came into this period on solid footing, we will continue to make tweaks to client portfolios based on the facts and circumstances presented. As we mentioned back in April after “Liberation Day,” we felt it was imprudent to completely overhaul client portfolios in response to an event so unpredictable as tariff negotiations. There was too much uncertainty, and making a material portfolio shift would be acting as if we know what the market is going to do next. We live in a world of possibilities, but we have to make decisions based on probabilities. We are weighing those probabilities every day.

We will continue to have conversations with our clients. By truly listening and understanding your needs, we will continue to attract and retain outstanding people to serve our families and our communities. We have never been more excited about what we’re building here at Red Door, and we are grateful for the trust you have put in us. We will never take that for granted – thank you.