The Entryway: Q1 2026 Market Update & Outlook

Market Snapshot:

After closing out 2025 on a strong note, investors and markets entered the new year with cautious optimism and meaningful momentum. The prevailing view was an expectation of continued strength in markets and the economy as businesses and the consumer had successfully navigated the new administration’s tariff policies, unemployment was still reasonably low, interest rates were likely to go lower, and the administration’s deregulation and tax policies were expected to further help companies and individuals. That optimism was quickly tested as the continued rapid advancement in AI models and products disrupted software stocks, private credit continued to be under the microscope, and a new and potentially prolonged conflict emerged in the Middle East.

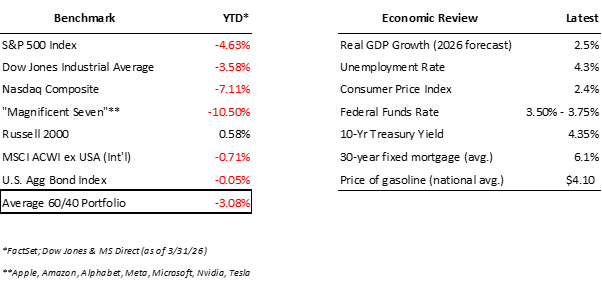

At the end of the first quarter, here is where major U.S. stock indices & economic conditions stood:

The US stock market started off the year very strongly with the S&P 500 hitting an all-time high of 6,978 on January 27th. However, these all-time highs quickly turned as the narrative around artificial intelligence and its’ potential impact on companies and employment accelerated, nervousness within some areas of the private credit market (more on this later), and anxiety around a potential war in the Middle East lead to the S&P 500 retreating ~9.5% from its’ all-time high thru March 30th. In an unusual turn, this sell-off was actually led by the same companies that have powered the market higher over the last 10 years, the Magnificent Seven, which was collectively down ~11% in Q1 2026.

Patient investors were rewarded on March 31st with the S&P 500 increasing +2.91% in a single trading day marking its’ best single-day performance in over 10 months and served as a textbook example of why “time in the market” beats “timing the market”. In fact, over the last 25 years (2001 – 2026) the average annual return of the S&P 500 is ~9.85%/yr. However, if an investor just missed the 10 best performing days over that same 25-year period their annual return would have been reduced from ~9.85%/yr down to ~6.35%/yr — a staggering 35% reduction by simply missing just 0.15% of the trading days over that 25-year span.

We believe this continues to reinforce and remind all investors that the key to long-term success is not timing the market and trading but more focusing on the things you can control: understanding your near-term and long-term goals, customizing your asset allocation around those goals, and staying disciplined to your plan. This approach allows you to stay appropriately invested throughout the inevitable storms, while providing structure and discipline to your investments that should yield better results and more peace of mind.

Macro Update, the Fed, Inflation, and Interest Rates

On February 28th, U.S. and Israeli forces launched Operation Epic Fury (and Roaring Lion) — a series of coordinated strikes targeting Iran’s leadership, nuclear facilities, ballistic missiles & drone infrastructure, and other military assets. Almost immediately, Iran closed the Strait of Hormuz, the narrow waterway through which approximately 20% of the world’s oil supply flows. The International Energy Agency characterized the ensuing supply disruption as the largest in the history of the global oil market. Almost overnight, Brent crude prices surged and gasoline prices at the pump climbed sharply, with the national average for a gallon of gas increasing to $4.10 – an ~37% increase.

While the increase in oil prices is likely temporary, this does reintroduce an inflationary force that the Federal Reserve had largely been gaining ground against. Inflation — which had been running near 2.4%, is now expected by many economists to approach 3% or higher in the coming months as higher energy costs filter through airfares, shipping, food production, and the broader goods and services economy.

The Fed held rates steady at their March meeting (the federal funds rate currently sits at 3.50% to 3.75%), while acknowledging that the conflict has meaningfully complicated their path forward. Prior to the conflict, markets were pricing in two rate cuts in 2026. Today, markets have dialed those expectations back to one — or possibly no rate cuts in 2026. While Chair Powell’s term ends in May, and new Fed-Chair Kevin Warsh is expected to be more constructive on lowering interest rates, the ongoing conflict in the Middle East and the resulting increase in the world’s input costs is a new wrinkle that potentially complicates the interest rate path moving forward.

On the employment front, February’s jobs report delivered an unpleasant surprise with the U.S. economy shedding 92,000 jobs in the month, and revisions to December and January subtracted an additional 69,000. The unemployment rate edged up to 4.3%, though weekly jobless claims have remained relatively subdued heading into April, suggesting the labor market has not fundamentally broken down. While the unemployment rate has marginally ticked higher, it remains meaningfully below the 50-year historical average of approximately 6%, and the economy continues to generate jobs in healthcare, education, and construction.

While we are less concerned about the current employment picture, we are continuing to monitor the more concerning “K-shaped economy” that has been developing for years across America. Simply put, those who own assets — homes, equities, businesses — have had a better ability to absorb inflation and still grow while those who do not own assets and are financing daily life with debt are experiencing a decidedly different economy / outcome. For instance, auto loan delinquencies have risen to 5.02%, roughly 40% above the long-term average and credit card delinquency rates have climbed materially from their 2022 lows across both lower- and higher-income zip codes. This divide and some of the potential cracks in the economy & credit markets are things we will continue to monitor as we build out and/or tailor client portfolios.

While there are numerous aspects within the economy & business community that give us much optimism, we believe it makes sense to be cautious and tactically de-risk portfolios where necessary. A recent positive development is that as of the time of this writing, there has been a two-week ceasefire agreed to between the United States and Iran as they continue to push towards a workable peace agreement. This is an encouraging development as I know we all hope there is a sustainable solution that makes sense for the world. Simply put, the longer the Iran war goes on the higher probability of economic and market issues. We are watching closely and will continue to make any investment changes if needed.

A Note on Private Credit: There’s a difference

Many may have seen headlines in recent months about private credit, with names like Blue Owl, Blackstone, and Apollo appearing prominently in the financial press. While many of our clients do have some exposure to private credit investments, it is important to understand the differences between those funds and the funds that our clients may have exposure too.

First, private credit is a broad term used to describe loans made directly by non-bank lenders. Over the past decade, the asset class grew from a niche institutional product into a roughly $2 trillion market, attracting capital from pension funds, endowments, other institutional investors and, increasingly, individual investors. Firms like Blackstone, Apollo, and Blue Owl have historically been some of the biggest players in this space.

Recently, there has been more scrutiny given to those groups because a material percentage of the collateral backing their loans are software companies. This “software concentration” has caused some anxiety from investors as artificial intelligence companies like OpenAI (ChatGPT), Anthropic (Claude), Google (Gemini), xAI (Groq), etc. develop innovative products that provide many of the same services & efficiencies as traditional software companies. In addition, many of these loans extended by Blue Owl, Apollo, and Blackstone are “subordinate / junior” debt which is a type of loan that sits lower in the payback waterfall than senior secured debt. The bottom line for those strategies is that the loans they are making are generally subordinate debt positions and to predominantly software businesses who may now have less resilient revenues and profits (because of the rapid evolution / advancement of AI products and services).

The keys differences between those strategies and the private credit strategies that our clients may have exposure to are the following:

- The loans the private credit groups we have investments in are almost all senior secured loans (i.e., they are in first position to take back the collateral if needed)

- These loans are backed by “hard assets” like real estate, infrastructure, equipment, receivables, royalties, etc. vs. less reliable cash flows from businesses currently being disrupted by AI

Lastly, and most importantly, your asset allocations are completely customized around your specific needs, goals, and circumstances. In other words, we work with every client to build out a financial plan / roadmap where we understand your financial situation, when you may need money / distributions, and build in liquidity within accounts to ensure that dollars you may need in the near-term are in extremely low risk investments like cash, money market funds, and US Treasuries. Generally speaking, we work to have 2.5 – 5 yrs worth of your near-to-medium term distributions in risk-free investments like cash or T-bills.

While we continue to believe there will be stories in the financial press that highlight various issues within “private credit”, it is important to understand there are great managers within the private credit space, and we have purpose-built portfolios around your specific facts and circumstances.

Thank you!

In closing, we want to thank you for your trust, and we are grateful for the opportunity to serve you and your families. We work incredibly hard to attract and retain great individuals who exhibit the entrepreneurial spirit, relentless drive, and servants heart we’re looking for within our firm, and we believe our people and our culture are critical to our collective success. As always, if you have any questions please do not hesitate to reach out and we look forward to the year ahead!