The Entryway – 2023 Q3 Update

Market Check-in

As summer comes to a close, many families are embracing the upcoming school year – new goals, commitments, schedules, after-school hobbies, etc. In short, change is upon us. Almost two-thirds of the way into the year, markets are also experiencing some change – most noticeably with inflationary pressures fading and GDP expectations rising. In turn, market participants are changing their perspective from a “hard landing” where the Fed must soon cut interest rates to the likelihood of higher rates for longer. Interest rates on longer maturity bonds are rising, and risk assets are selling off. For instance, in August the 10-year Treasury yield rose from ~3.75% to ~4.35% (a more than 15% increase), and the S&P 500 has pulled back more than 5% during that time as well. Despite this slight pullback, broad market indices continue to be positive for the year.

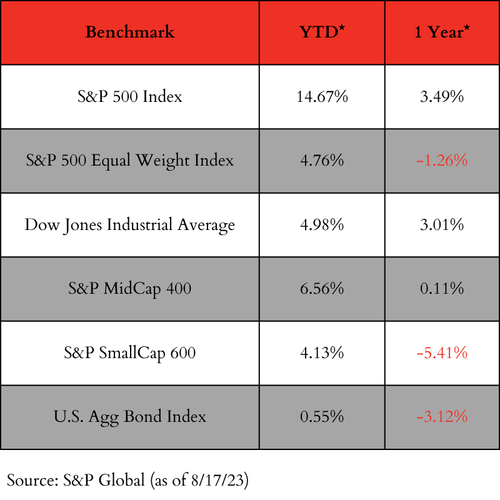

As of Aug. 17, here is where the major indices stood:

There are a couple of items to note here. First, investors have experienced quite the ride over the last 12 months as markets have been highly volatile and returns minimal. For instance, over the last year an investor who was ~50% stocks and 50% bonds was essentially “flat.”

The second item to note is the disparity between the performance of the S&P 500 Index and the S&P 500 Equal Weight Index. As a reminder, the S&P 500 Index is cap-weighted, which means companies with higher market value have more of an influence over the price of the index versus companies of lesser value. The S&P 500 Equity Index assigns the same percentage weighting to all 500 companies within the index. The punchline here is that there are a select few companies that are driving almost all of the market returns YTD.

In fact, the top seven companies in the S&P 500 account for ~30% of the entire S&P 500 Index – Apple, Alphabet (Google), Meta (Facebook), Microsoft, NVDIA, Amazon and Tesla. These are all incredible businesses that have in some fashion transformed the way we operate and consume products and services. However, this type of concentration is something to monitor closely. It can be painful when unwound. (See what happened in 2022!)

Lastly, we believe that stocks are fully valued to overvalued as the earnings per share for companies in the S&P 500 has declined in 2022 while the multiple market participants are willing to pay for those earnings has expanded. For example, the S&P 500’s price-to-earnings ratio is sitting around 20 times the next 12 month’s earnings or ~20% higher than the 25-year average. While it is not unusual in recent years for price-to-earnings ratios to be this high, the multiple that investors are willing to pay is generally not nearly this high when risk-free assets – cash and US Treasuries – pay you about 5% to 5.5%.

The Fed and the economy

To date, the Federal Reserve has raised rates four separate times this year with 0.25% rate hikes in February, March, May and July. Hikes were paused in June. Currently, the Federal Funds Rate stands at 5.25% to 5.50%. As previously mentioned, the Fed raises interest rates in order to try and slow down the rate of inflation (i.e., the acceleration in price of the goods and services we consume) by slowing down the economy. Higher interest rates have many intended and unintended consequences. For consumers, one of the most straightforward and fundamental impacts of higher rates is the increased cost of capital (i.e., how much it costs you to borrow money). It eventually makes it unaffordable for many to finance cars and houses or reinvest in your business. As a result, people spend less. If spending is down, so is revenue, which eventually leads to layoffs to compensate for the reduction. As people lose jobs, they are uncertain about their future and have less money to spend. This creates a self-reinforcing loop that slows the economy in a material way.

However, there are a couple of caveats here that are important. First, this process operates with a lag. The last thing an employer wants to do is to terminate an employee. Generally speaking, it is costly for a business owner to attract, train and retain employees. Therefore, firing an employee is generally an employer’s last option. Currently the unemployment rate in the U.S. is 3.5%, the lowest in more than 50 years.

Second, consumers and businesses came into this tightening cycle in a strong position. Consumers were coming out of COVID-19 with strong balance sheets as many people refinanced their debts into long-term, fixed interest rates that were at historical lows. Additionally, over the last two to three years, employees have seen a rise in wages to help offset some of the increase in their cost of living. While the tightening campaign will eventually catch up to the consumer, it has not done so in a meaningful way yet. Businesses were no different in that many recognized the historic low-rate environment they were living in and chose to refinance near-term debts into long-term, fixed debts at very low interest rates.

The last item that is really counter-balancing this restrictive monetary policy is the fiscal stimulus and spending that is still working its way through the system. For instance, the Inflation Reduction Act (IRA) was passed in 2022 and directs federal spending toward reducing carbon emissions, lowering healthcare costs, funding the IRS and improving taxpayer compliance. The IRA directs nearly $400 billion in federal funding. In addition, the CHIPS Act was also passed in 2022 and contains more than $50 billion to support the domestic semiconductor industry. While these are “headline” numbers, there are significant investments and spending behind these as companies are vying for these subsidies. In short, this fiscal spending is counteracting some of the monetary tightening that is taking place. Ultimately the tightening campaign will win, but it’s taking longer than most expected.

A Constant Reminder

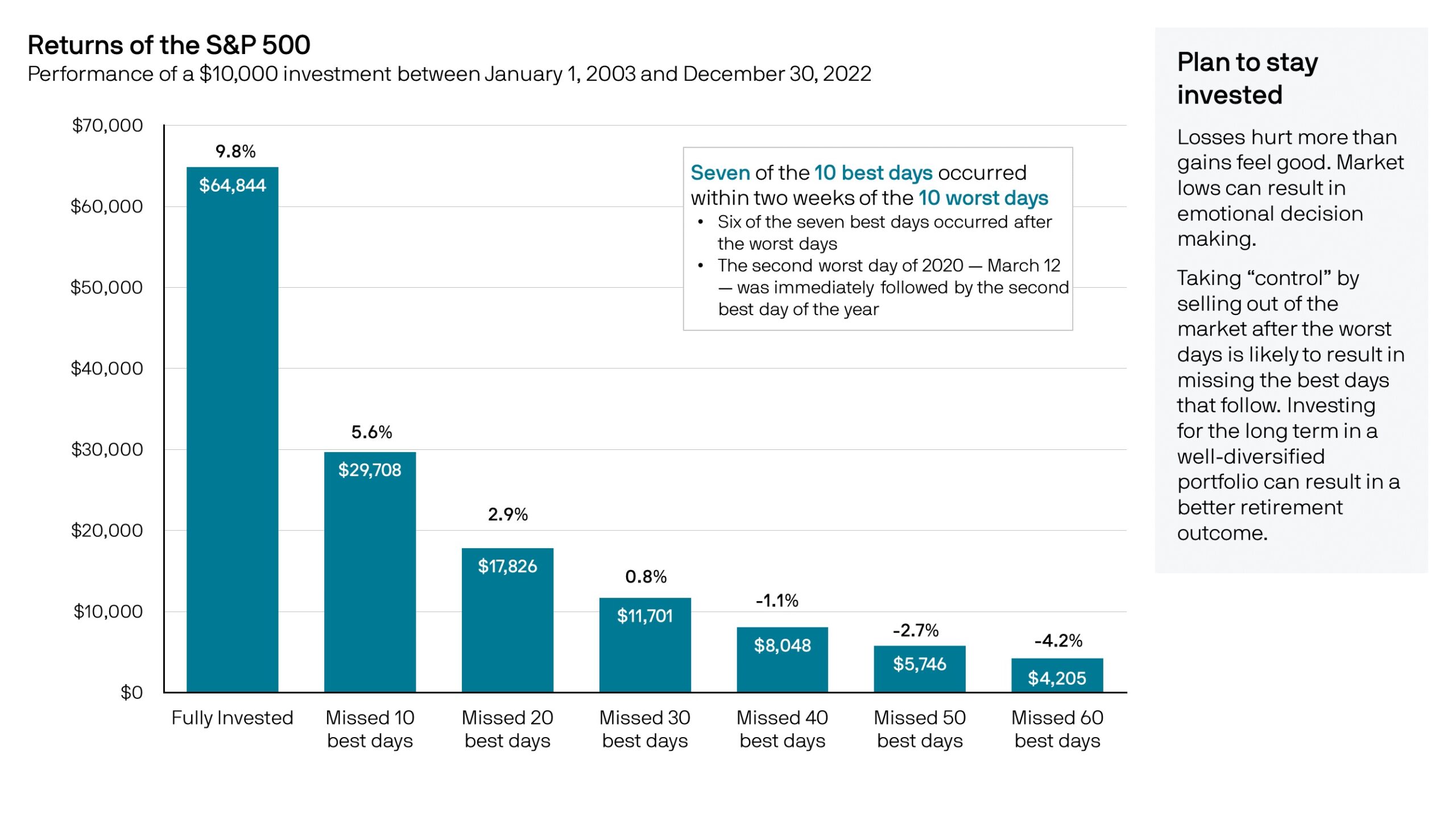

The toughest component of investing is being patient, staying committed to your plan and ignoring the urge to “time the market.” Our job is to protect our families the best we can and preserve their hard-earned dollars. As a result, we spend countless hours researching and reading about markets. Ironically, the more you read, the humbler you become. Similarly, the more perspective you gain about markets and investing, the more you realize the toughest component of investing is being patient, blocking out the noise and staying committed. A recent JP Morgan study provides a great illustration where they studied the past 20 years’ worth of market returns of the S&P 500. The historical annual return during that time period is ~10% per year. However, if you just take out the best 10 days during those 20 years (or less than 0.20% of trading days), your annualized return drops from 10% to 5.6%. In addition, if you missed the best 30 days during those 20 years (or less than 0.60% of trading days), your return drops from 10% per year to 0.80% per year!

We know you may get tired of us continuing to say this, but it is true – we need to control the controllables. We cannot control markets, politicians, interest rates or inflation. However, we can control our communication with you, the plans we lay out, our understanding of your specific needs and then tailoring your investments around those needs. Once we do that, we must stay invested while making tweaks to strategies along the way.

As we all go through whatever changes lie ahead, remember that we are here for you as an added resource for you and your family. We all know that life is full of uncertainties. We welcome these challenges and are confident in the collection of individuals we have assembled on your behalf to serve you. We appreciate the trust you have put in us, and we look forward to the remainder of the year!