The Entryway – 2023 Q1: Market Update & Outlook

Market Check-In

After a bull market that lasted for more than a decade coming off the heels of the global financial crisis of 2008-09, markets experienced a significant pullback in 2022. Unfortunately, whether you were a very conservative investor with a high concentration of high-quality bonds or a more aggressive investor with a high concentration in growth stocks, you experienced a market sell-off that has rarely happened in history. For example, there have only been four other times in the last 100 years where both U.S. Treasuries and the S&P 500 finished the year down – 2022 became the fifth year on record where this happened.

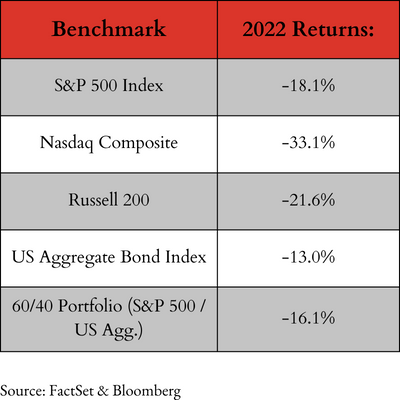

Here is where the major indices finished 2022:

The S&P 500, the Nasdaq Composite and Russell 2000 all logged their worst annual declines since 2008, and the S&P 500 had its seventh worst year on record stretching back to 1928. What made this year even more painful for investors is the fact that bonds – which traditionally do well when the stock market suffers – also experienced material declines. In fact, the U.S. Aggregate Bond Indexes’ -14.6% return was its’ worst year on record stretching back to 1976.

With a few exceptions, especially a few months in 2020 during the COVID-19 outbreak, the overall period since the end of the global financial crisis was one in which worry was minimal and optimism prevailed. Up until late 2021 / early 2022, we lived in a period of low inflation, cheap access to capital (i.e., low rates), increased “spending” (both fiscal & monetary) and solid economic growth (slow but steady). As a result, these were golden years for investors as this low inflation / low-rate environment encouraged people to borrow and spend, provided corporations with access to cheap capital to reinvest and grow, and pushed up all sorts of asset prices as individuals and institutions had limited alternatives to risk assets.

To illustrate this period, look at the S&P 500. The historical annual return for the S&P 500 from 1928 until the global financial crisis’ low (March 2009) was ~10%/year. From March 2009 until the end of 2021, the annual return for the S&P 500 was ~15.5%/year or 55% higher than normal during those 12+ years. In our opinion, this is a straightforward illustration of what ultra-low interest rates can do to asset prices, which includes stocks, houses, private equity, etc. The question we have been asking ourselves for the past year or so is: Are we entering into a new, sustained period where the economic environment looks vastly different than the last 10-12 years?

Market Outlook: A potential sea change

Since 2008, the Fed has kept interest rates extremely low by historical standards and purchased securities (mainly Treasuries and Mortgage-backed securities), which increased the amount of money in the system to stimulate borrowing. What are some impacts low interest rates have?

- The rates make it cheaper for people to buy things on credit and for companies to invest in property, plant and equipment.

- The cost of capital for businesses is less, and therefore, they are more profitable.

- The rates mathematically increase the fair value of assets, i.e., the discounted present value of future cash flows is higher.

- As asset prices increase, companies and consumers are more confident to spend, causing even more demand.

In short, these borrow-friendly policies stimulated demand and encouraged risk taking. For over a decade, the Fed was able to continue with these policies without causing any sort of inflationary pressure. When the COVID-19 pandemic caused much of the global economy to shut down, the Fed doubled-down on these policies and within weeks put into effect an amplified version at a much larger scale. In addition, the federal government increased spending in a variety of areas, sent direct payments to consumers, backstopped businesses, and granted abundant debt relief or abatement.

It was at this point that these easy monetary conditions combined with disrupted supply chains (both from the pandemic and later the Russia/Ukraine war) finally caused inflation to rear its head in the spring/summer of 2021 and accelerated into late 2021 and mid-2022, hopefully peaking in June 2022 at 9.1% year-over-year.

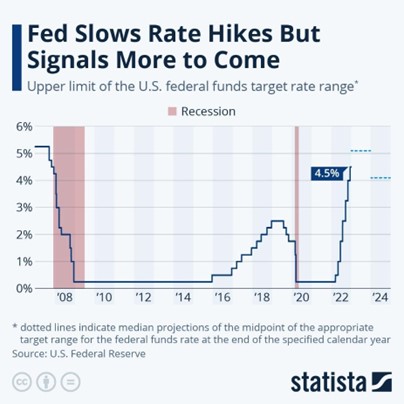

In response to the highest inflation in over 40 years, the Federal Reserve finally conceded that inflation was not “transitory” and began aggressively tightening monetary policy in March 2022. The Fed knew that they were behind the curve and had allowed these easy conditions to last too long and felt forced to increase the federal funds rate from 0-0.25% all the way to 4.25-4.50% or by over 400% in nine months, making this the most aggressive interest rate increase on record.

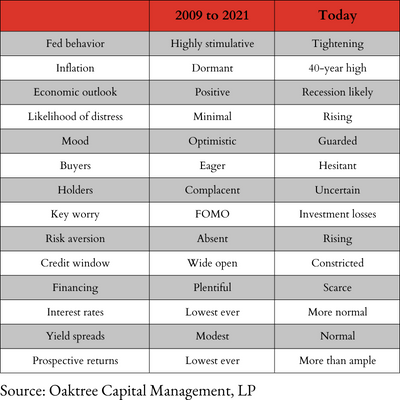

As a result of higher inflation and higher rates, we have now entered a new environment where monetary conditions are tight. Banks are less willing to lend or are lending on less favorable terms, people are less optimistic and less likely to spend, and people are reassessing their risk appetite as they feel less certain about their future. In short, this environment feels much different than the 2009-21 time period. We recently read a memo from Howard Marks, famed investor and co-founder of Oaktree Capital Management, who compared this change in environment:

If we are entering into a new environment where inflation and interest rates remain elevated from previous decades, we also must evolve our investment strategies to meet these new realities. While change can be difficult and can cause concern, investors are not out of options. For one, control what you can control. We can control our communication, our planning, our understanding of your needs, and tailor your investment and planning to give you the highest probability of success. In addition, we will not stand flat-footed and continue to implement investment strategies that were best suited for the 2009-21 market environment.

For instance, over the course of 2022, you have seen us shift the significant majority of our stock dollars into value companies that are more stable, produce more cash-flow and are more resilient when the cost of capital is higher. We also moved into short-term individual bonds and will continue to lock in rates of return at 4.5-4.75% (often risk-free individual U.S. Treasuries). We can also utilize Schwab’s platform to get a healthy rate of return on cash of around 4-4.25%. Lastly, we will continue to search and vet unique alternative investments that should continue to outperform traditional assets in this new environment.

While we may be entering a new environment and this year has been tough, we are resolute in our commitment to our processes, we continue to retain and hire the highest quality people and we provide a variety of services for the families we serve. We are looking forward to 2023 and look forward to the meetings and conversations ahead where we can hopefully continue to provide a steady hand during uncertain times, continue to help plan around your specific needs and continue to find investment solutions that give you the highest probability of sustained success.