The Entryway – 2022 Q4: Market Update & Outlook

Market Check-In

Global markets continued their decline in the third quarter as inflation remained near 40-year highs, geopolitical tensions continued to escalate, and the Federal Reserve continued to raise interest rates consistently and aggressively. While tough to remember, the third quarter got off to an optimistic start with some costs, like gasoline prices, materially falling, and inflation peaking in June at 9.1% and second quarter earnings being more resilient than expected. All these ingredients added up to a hopeful “Fed pivot,” in which the Fed would slow the pace or degree of their interest rate increases and companies would weather the storm. Market participants began pricing in a potentially “softer landing” than previously expected, and asset prices moved up accordingly.

However, in late August, this narrative was put to bed when Fed policymakers had their annual retreat in Jackson Hole where Fed chair Powell clearly stated unwavering commitment to fight and lower inflation regardless of the pain it may cause to markets, unemployment and businesses in the short run. From that point, markets reversed their near-term trend and began repricing assets to account for more consistent and more aggressive interest rate hikes by the Fed. This anticipation by the market was proven out when the Fed met in September and again raised interest rates by 0.75% ̶ bringing the federal funds rate to 3-3.25% and indicating that the federal funds rate would likely increase to 4-4.50% by year’s end. By the end of the third quarter, the major market indices all made lower lows and the average 60/40 investor was down over 21% as of the end of September.

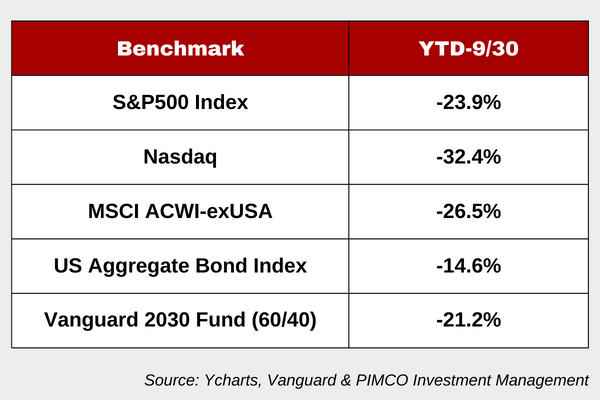

As of the end of the third quarter, here is where the major indexes stood:

In short, traditional stock and bond investments continued to sell off in concert, and last quarter marked the third straight quarter of declines in both major asset classes. This is the first time since 1976 that both stock and bond prices have fallen for three consecutive quarters.

Headwinds, Fed Policy, Labor Markets and Interest Rates

To date, companies, families and investors are dealing with many headwinds – higher prices, higher cost of capital, lack of labor, a strong dollar and general geopolitical uncertainties. While these various factors are all playing a part in the sell-off in asset prices, the interplay between high inflation and Fed policy is the driving force behind the decline in asset prices.

As a reminder, the Federal Reserve has a dual mandate: maximum employment and price stability. In other words, their stated job is to influence monetary policy to find an equilibrium between a healthy economy / labor market and stable prices. While inflation seems to have peaked, it is not falling fast enough for the Fed to begin pivoting their policy and “core inflation” (i.e., CPI excluding food & energy) is continuing to hit new highs each month. The Fed is in a tough spot where they are committed to continue their policies until inflation materially decreases and trends back down to the 2-4% level. However, the geopolitical issues are greatly impacting energy markets, a very strong labor market is continuing to put pressure on the cost of goods and services, and the inherent lag in how housing costs are calculated in the inflation prints are putting continued upward pressure on inflation numbers. While all these factors have a direct impact on inflation and Fed policy, let’s look at the labor market.

Labor markets in the U.S. remain tight. The unemployment rate sits at 3.5%, matching its lowest level in the last 50 years, and there are two job openings for every unemployed person in the US. While this is good news, employers are having to compete even harder to attract and retain employees. Pay raises are a positive thing, but this generally causes business owners to pass along this cost and increase to the prices of the goods and services they are selling. In addition, people with higher wages can mostly afford these increased costs, potentially creating a self-reinforcing feedback loop that may cause inflation to stay stubbornly high and complicate the Fed’s policy.

Currently, the Fed is fighting against this trend by consistently and aggressively raising interest rates to reduce demand. Why? Because 70% of the GDP in this country is based on consumer spending, which businesses around the world count on to support their operations and growth. The thought is that at some point the cost of capital, i.e., interest rates, gets high enough to negatively impact consumer behavior and people spend less. When consumer demand and confidence wane, enough people will spend less and ultimately employers will start laying off employees. While this will eventually work, it is extremely painful for all parties as this drives up unemployment and depresses asset values, e.g., stocks, bonds, real estate, private business valuations, etc. In short, the Fed is trying to thread the needle and perform surgery, and instead of having a scalpel, they have a chainsaw.

What Are We Doing and What’s Next

During the third quarter, we continued our systematic shift to a more defensive posture by lowering even more of our stock exposure and shifting those dollars into a long/short strategy that has significantly less volatility than stocks (70% less volatility than S&P 500), low overall correlation, and better downside protection provided. We continue to lean into the alternative investment space and believe this area will continue to provide better downside protection and higher opportunities to outperform on a relative basis.

In addition to alternatives, we continued to move more client dollars into individual, short-term U.S. Treasuries where we are consistently seeing and “locking in” yields of 4%+. Remember, the price of these individual bond ladders will continue to move up and down as the Fed raises or lowers interest rates, but the bottom line is that as long as the U.S. government does not default on their debt before the maturity period (generally 3-1212 months) you are guaranteed to get the stated yield to maturity – averaging about 4% at the moment.

Lastly, we continue enhancing our cash position by making the best of a bad situation and taking advantage of Schwab’s preferred money market funds. This cash investment currently yields 2.95% and has daily liquidity.

In short, this has been an extremely tough year and we expect the markets to continue to be volatile until the credit markets ̶ driven by interest rates ̶ calm down. Credit markets will only calm down once they have visibility on the Fed’s policy, which is being driven by persistently high inflation.

When will this end? The highest probabilities for the Fed to change course is either for the inflation numbers to consistently start falling in a meaningful way or something in the financial plumbing of the system breaking because it cannot support higher rates. In either scenario, the Fed will likely reverse course, stop increasing interest rates and likely even cut rates. Once this happens, we expect asset prices to increase, and we will begin shifting our strategies back to a more offensive posture by shedding some alternative investments, cash and maturing bond proceeds into stocks.