The Entryway – 2024 Q3: Market Update & Outlook

After a strong first quarter in 2024, the broad market indices continued to post solid gains. However, during the second quarter there was a significant divergence between the average stock within the S&P 500 vs. the mega-cap technology stocks (referred to as the “Magnificent Seven”). For instance, the S&P 500 was +4.3% in the second quarter while the S&P 500 equal-weighted index was -2.6%. How does this happen?

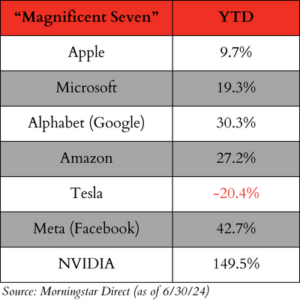

The S&P 500 is “market cap weighted” meaning the companies with the largest market cap or value have more influence or weighting within the overall index. Therefore, if equity markets are concentrated at the top with a handful of dynamic companies absorbing all the value, those companies will greatly influence an investor’s returns. We have written about this phenomenon for many quarters now, and this theme has only accelerated with the development and “spend” around artificial intelligence as many of the perceived beneficiaries are these same companies. At the end of the second quarter, the Magnificent Seven (Apple, Amazon, Alphabet, Meta, Microsoft, NVIDIA and Tesla) were continuing to drive the broad markets higher with those companies by 33% on average, year to date. By contrast, the remaining 493 companies in the S&P 500 gained 5% on average through the end of the second quarter.

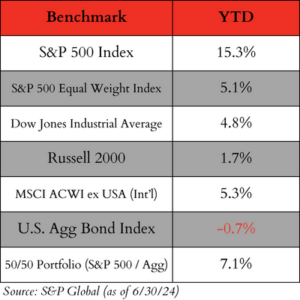

At the end of Q2 2024, here is where the major public market indices stood versus the Magnificent Seven:

While our clients own stocks in the majority of these companies and we are happy with these “top line” numbers, there are a couple items to highlight here. First, just like in 2023, the total return of the S&P 500 continues to be extremely narrow with many companies struggling while the top companies continue to outperform. The performance of the various stock indices confirms the underlying weakness of many companies versus the mega-cap tech companies with the S&P 500 Equal Weight Index underperforming its market cap weighted index by ~10%, the Dow Jones Industrial Average underperforming the S&P 500 by ~10% and the Russell 2000 underperforming by ~14%.

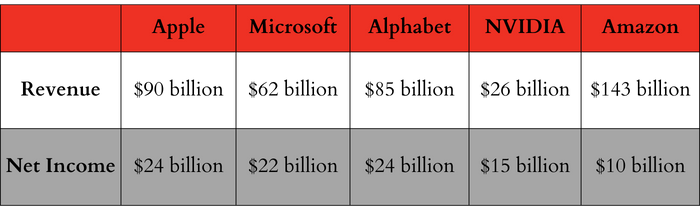

While many look back to the run-up of the Nasdaq composite in the mid-to-late ‘90s as an applicable comparison, we see many differences. In our view, the biggest difference between then and now is these companies are exceptional businesses with real products and services that consumers value and pay for. They are highly profitable business models (minus Tesla), and the leaders of these organizations continue to reinvest their significant profits back into their business for future innovation and growth.

For some perspective, here are the most recent quarterly revenue and net income numbers for five of the Magnificent Seven companies:

While these are enduring, successful businesses we believe investors should have exposure to it are becoming a crowded trade and can lull investors to sleep. The bottom line is there is a variety of uncertainties within this market, and the outperformance of a few is heavily influencing the overall performance of the index. For instance, at the end of the second quarter, the top 10 companies in the S&P 500 represented ~37% of the entire S&P 500 market cap. This makes the overall market more susceptible to outsized moves (up and down) and heavily affects index valuations.

While we are thrilled to see asset prices rise for our clients, we continue to critically analyze the concentration risk in the stock market, the elevated current valuations, and how the current interest rate policy of the Fed, the economy at large, and the upcoming elections may impact companies and their earnings.

Market Outlook: The Fed, the Economy, Inflation and Interest Rates

Clearly the “experts” were wrong going into the year when they anticipated the Federal Reserve might ease rates up to six times in 2024. To date, these rosy forecasts have been wrong and persistent inflation has caused the Fed to hold interest rates at their 23-year high.

While there are some indicators like credit card and auto-loan delinquencies ticking up, the underlying economy within the United States remains solid. We always borrow the famous Ray Dalio quote that says, “One person’s spending is another person’s income.” In other words, the overall Gross Domestic Product (GDP) in the United States is ~70% consumer spending, so the U.S. needs people to work, earn a good living and make purchases. While the unemployment rate has edged up to 4% from a low of 3.4% set in April 2023, the unemployment rate now sits near 4% for the past two and a half years, the longest such stretch since the late 1960s. In addition, there are ancillary factors that are contributing to the strong consumer. For instance, most households took advantage of previous low interest rates to lock in low fixed rates. To date, ~90% of U.S. household debt is fixed, while floating rate debt and most other debts have low interest rates. Lastly, consumers and savers are taking advantage of the higher cash interest rates (most high-yield savings yield 5% and more), and these are additional dollars to spend.

In addition to the consumer, the government continues to spend. Over the past two to three years, the government passed the Inflation Reduction Act and the CHIPS Act, both of which pour billions of dollars into direct developments, incentives or credits. These direct dollars or incentives / credits tend to find themselves back into the economy via spending and revenue for companies, which allow them to retain their employees and even expand their wages. The caveat here is that these dollars / incentives must be productive or the positive impacts will be short-lived.

As investors, we must continue to customize your asset allocation around your personal needs and stay invested in a variety of high-quality assets, such as stocks, bonds, cash and alternative investments. This is what we are currently doing for families and will continue to evolve our strategies as market dynamics change. Despite these changes, we are extremely confident in the people we have at our firm and believe that our process gives you a high probability of meeting and exceeding your goals.

Lastly, we all know that 2024 is an election year. With any election year, there will be high emotions and varying debates on what is best for our country. From a historical perspective, whoever is in the White House has little impact on investment returns over the medium-to-long-term.

A Constant Reminder

One of our main jobs is to protect our families the best we can from market volatility and emotional mistakes. To that end, we spend much of our time listening, asking questions to better understand your specific needs and building a process around those needs. While it is never easy, there is great satisfaction and reward for those who can stay the course and consistently make logical decisions. Here are some great reminders:

- Control the controllables. This starts with having transparent and direct conversations. We must understand where you are and where you want to go. This starts with candid conversations. Not only does this continue to build trust within our relationship, but this information helps us partner together to build a custom plan for you and your family. Once this foundation is laid, we then can build out a plan and reverse engineer solutions for your stated needs – how much cash do you need, what is your income shortfall and how much liquidity should we have on hand, what rate of return do you need to meet your goals, etc. These conversations are the bedrock of our relationship, they inform our asset allocation work, and hopefully lead you to a more fulfilling and less stressful life.

- Stay patient and disciplined. Money, markets, the economy and elections, for example, are emotional and your circumstances will always change. However, don’t let change or things out of your control negatively influence your peace of mind and improperly influence your decision-making. As long as we collectively work together and have honest conversations, we can continue to develop and implement disciplined processes that will keep you and your family on track to meet your goals.

- Communicate. One of the only guarantees in life is change. Change is inevitable, and it can be empowering if planned appropriately. We feel confident in the people we have within our firm to deliver solutions for the families we serve, but we must know what problem to solve or goal to achieve. This is a two-way street, and we will continue to work hard on our end to communicate effectively and build out custom strategies that endure over the decades.